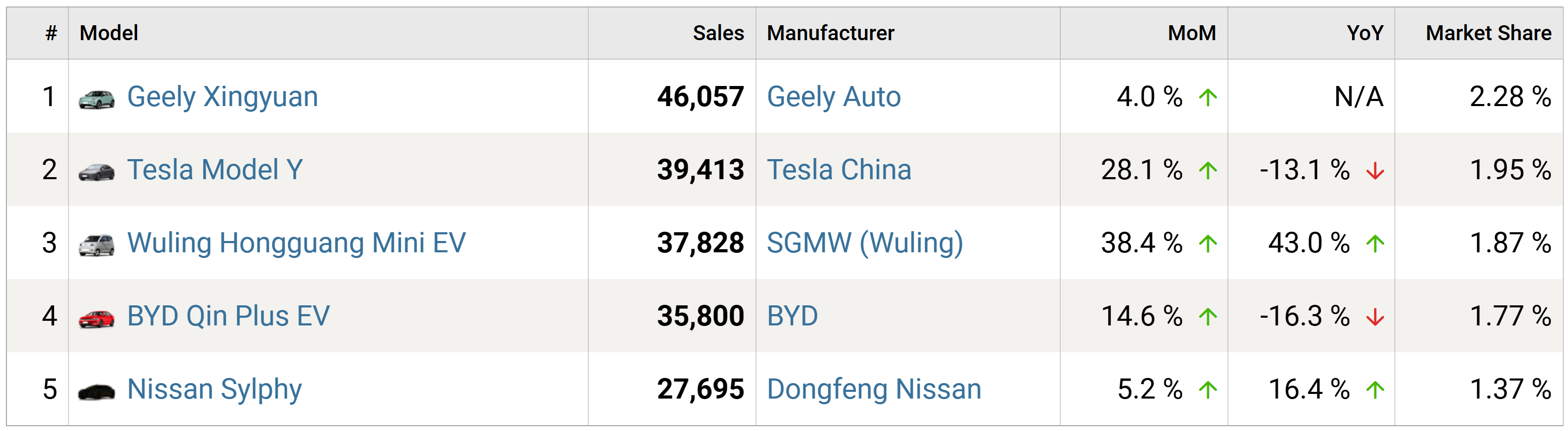

Individual EV model performance highlights market preferences and competitive dynamics.

Top EV Models by Sales Performance in China Market

Strategic Market Analysis

Key insights from comparative market dynamics

Scale vs Premium Strategy

China drives volume through affordability, with average prices of $15,000–$25,000 and sales surpassing 11 million units annually. In contrast, the U.S. targets the premium segment, averaging $45,000–$55,000 per vehicle, achieving 1.3 million sales with higher margins.

Manufacturing Approach

Chinese leaders such as BYD rely on vertical integration and scale efficiencies to reduce costs. U.S. automakers prioritize innovation, software integration, and brand positioning to justify premium pricing.

Infrastructure Philosophy

China’s 2.5 million public chargers reflect a dense, urban-focused strategy that supports mass adoption. The U.S., with about 140,000 chargers, emphasizes highway corridors and home charging to serve suburban markets.

Global Impact

China produces 60% of the world’s EVs and dominates battery supply chains, setting the pace for global affordability. The U.S. shapes industry standards through advances in autonomous driving and the influence of premium brands.

Consumer Behavior

Chinese buyers value low cost and urban practicality, favoring compact EVs. U.S. consumers prioritize range, performance, and size, driving demand for SUVs and trucks.

Innovation Focus

China leads in battery chemistry, manufacturing efficiency, and charging solutions, while the U.S. advances in software, autonomy, and user experience as key differentiators.

Key Strategic Takeaways

Market Size Disparity: China's 8.5:1 EV sales advantage underscores how government subsidies, lower production costs, and strong domestic demand have accelerated mass adoption.

Divergent Price Strategies: Chinese EVs are positioned as affordable and widely accessible, while U.S. models lean toward premium, high-margin offerings—reflecting two fundamentally different market philosophies.

Infrastructure Edge: With an 18:1 lead in public charging stations, China reduces consumer range anxiety and supports faster adoption, while U.S. infrastructure growth remains comparatively limited.

Technology Leadership Split: China holds a dominant position in battery supply chains, cost efficiency, and scale, whereas the U.S. maintains leadership in software integration, connectivity, and autonomous driving innovation.

Policy-Driven Futures: Both nations are targeting 50% EV market share by 2030, but China pursues rapid expansion through affordability and infrastructure, while the U.S. focuses on innovation and premium technology.

Potential Convergence: Despite divergent strategies, both markets are likely to align in the long term as cost efficiencies improve in the U.S. and China invests more heavily in advanced software and autonomy.